ITR Forms for A.Y. 2019-20 : An Analysis of amendments and additional disclosure requirements

CBDT has vide Notification No 32/2019-Income Tax Dated 01/04/2019 released the new ITR Forms for AY 2019-20. While there is no change in ITR-1 (SAHAJ) meant for salaried assesses, there are some changes in ITR-2,3,5,6 and 7 for the Assessment Year 2019-20 with some additional reporting requirements for directors, shareholders of unlisted shares and for companies. Here is a detailed analysis of the amendments in rule as well as the additional reporting requirements.

Applicability of Forms

| Applicability | Form No. |

| For individuals being a resident (other than not ordinarily resident) having total income upto Rs.50 lakh, having Income from Salaries, one house property, other sources (Interest etc.), and agricultural income upto Rs.5 thousand | ITR-1 SAHAJ |

| For Individuals and HUFs not having income from profits and gains of business or profession | ITR-2 |

| For individuals and HUFs having income from profits and gains of business or profession | ITR-3 |

| For Individuals, HUFs and Firms (other than LLP) being ordinarily resident having total income upto Rs.50 lakh and having income from business and profession which is computed under sections 44AD, 44ADA or 44AE | ITR-4 SUGHAM |

| For persons other than,- (i) individual, (ii) HUF, (iii) company and (iv) person filing Form ITR-7 | ITR-5 |

| For Companies other than companies claiming exemption under section 11 | ITR-6 |

| For persons including companies required to furnish return under sections 139(4A) or 139(4B) or 139(4C) or 139(4D) only | ITR-7 |

| Verification of Return | ITR-V Acknowledgement |

Amendments in Rule 12 of Income Tax Rules, 1967

ITR-1 (SAHAJ)

As per the said notification, Rule 12 has been amended to make the following changes. ITR-1(SAHAJ) cannot be filed by an Individual who:

- has claimed deduction under section 57, other than deduction claimed under clause (iia) thereof;

- is a director in any company;

- has held any unlisted equity share at any time during the previous year;

- is assessable for the whole or any part of the income on which tax has been deducted at source in the hands of a person other than the assessee.

ITR-4(SUGAM)

From AY 19-20, ITR-4 is applicable only to individuals, HUF and Partnership firm (other than LLP) which are ordinarily resident in India. ITR-4 cannot be filed by a person:

- has assets (including financial interest in any entity) located outside India;

- has signing authority in any account located outside India;

- has income from any source outside India;

- has income to be apportioned in accordance with provisions of section 5A;

- is a director in any company;

- has held any unlisted equity share at any time during the previous year;

- has total income, exceeding Rs. 50,00,000;

- owns more than one house property, the income of which is chargeable under the head “Income from house property”;

- has any brought forward loss or loss to be carried forward under any head of income;

- is assessable for the whole or any part of the income on which tax has been deducted at source in the hands of a person other than the assessee;

- has claimed any relief of tax under sections 90 or 90A or deduction of tax under section 91;

- has agricultural income, exceeding Rs. 5,000

- has income taxable under section 115BBDA;or

- has income of the nature referred to in section 115BBE;

ITR-7

As per the amended rule 12 of Income tax rules, 1961, ITR-7 is not applicable to business trust referred U/s 139(4E) and investment fund referred u/s 139(4F) of the Act.

Mode of Filing Returns

As per the amended Rule 12, in case an individual of the age of 80 years or more (super senior citizen) at any time during the previous year, and who furnishes the return in ITR-1 SAHAJ or ITR-4 SUGAM, return can be furnished-

- Electronically under digital signature; or

- Transmitting the data electronically in the return under electronic verification code (EVC); or

- Transmitting the data in the return electronically and thereafter submitting the verification of the return in Form ITR-V; or

- Paper form;

Before the amendment, an additional condition was there that income should not exceed Rs.5,00,000 and no refund is claimed in the return of income. However with the amendment in Rule 12, this condition is done away with.

Additional Reporting Requirement

ITR-2,3,5 and 7

-

Details regarding holding of unlisted equity shares at any time during the previous year.

The new forms require disclosure of unlisted equity shares of private limited companies as well as unlisted public companies in terms of number of shares and cost of holding held as opening balance, shares acquired during the year, number of shares transferred during the year and closing balance.

ITR-2,3 and 5

- PAN of the Tenant is mandatory, if tax is deducted under section 194-IB and section 194-I.

- In case of transfer of immovable property, furnishing PAN of buyer is compulsory where TDS has been deducted under section 194-IA

- Full value of consideration adopted as per Section 50C for the purpose of Capital Gain is calculated up to 105% of Value of Property as per stamp valuation authority.

- Schedule FA – Details of Foreign Assets and Income from any source outside India. The additional reporting are as below:

A2: Details of Foreign Custodial Accounts held (including any beneficial interest) at any time during the relevant accounting period

A3: Details of Foreign Equity and Debt Interest held (including any beneficial interest) in any entity at any time during the relevant accounting period

A4: Details of Foreign Cash Value Insurance Contract or Annuity Contract held (including any beneficial interest) at any time during the relevant accounting period

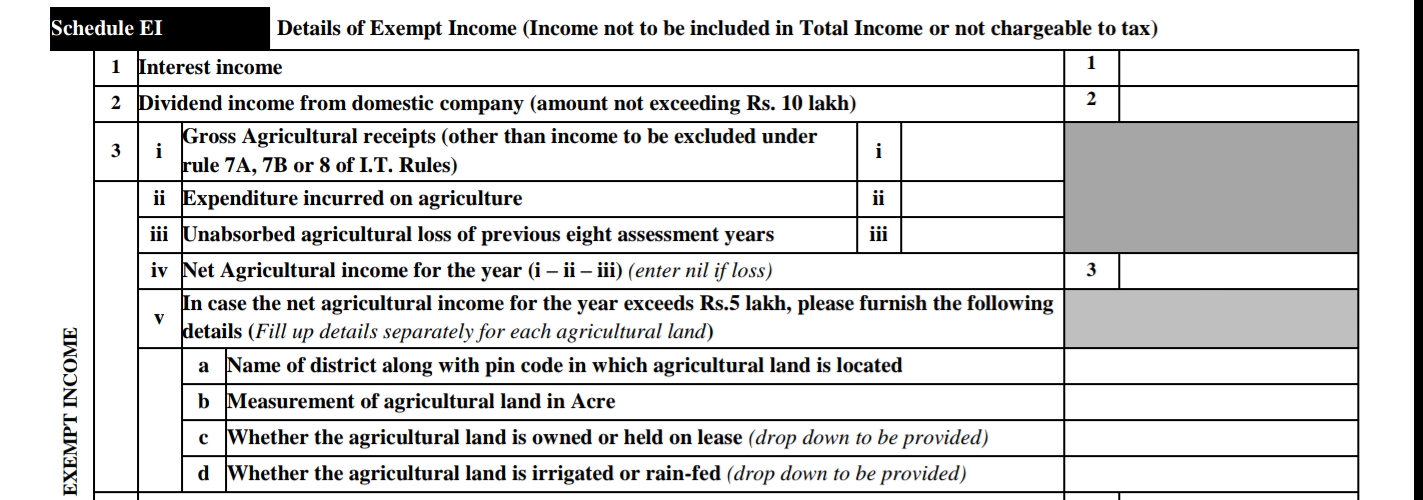

5. Agricultural Income exceeding Rs 5,00,000

ITR-2 and 3

-

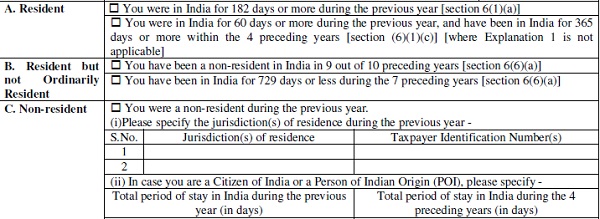

Residential Status

In the New ITR 2 and 3, comprehensive details about the residential status have to be given. In case of a non-resident, jurisdiction of his residence as well as his Taxpayer Identification Number has to be reported. In case of a person of Indian Origin or Citizen of India, Total period of stay in India (i.e. number of days) during the previous year as well as 4 preceding previous years has to be reported.

-

Details of Directorships in Company

As per the amendments, an individual who is a director in a company cannot submit ITR-1 (SAHAJ) or ITR-4(SUGAM) form. He must file ITR-2 or ITR-3 which requires reporting of details of the company in which he is a director. These include, name and PAN of the company, whether the shares are listed or unlisted and Director Identification Number of the director.![]()

ITR- 3,5 and 6

- Whether located in an International Financial Service Centre and derives income solely in convertible foreign exchange?

- Schedule GST – Information regarding turnover / gross receipts reported for GST included now in ITR 3 and ITR 6 also. Earlier it required was in ITR-4 only.

- PART A – P&L is divided into PART A – Manufacturing Account, PART A – Trading Account and PART A – P&L.

ITR-6

- In the case of companies, Date of Commencement of Business to be reported.

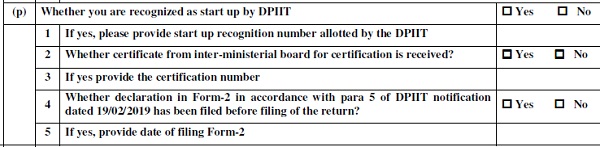

- Details of start up in ITR – 6 to be furnished

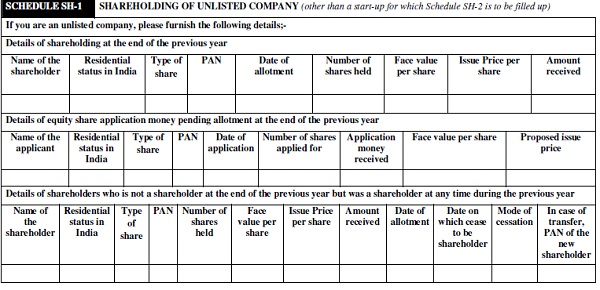

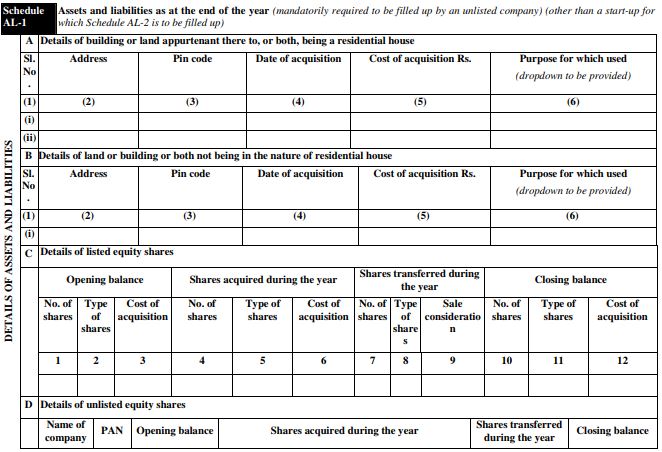

- In case of unlisted company, Schedule SH-1 and Al-1 to be furnished

In Schedule AL-1, following details to be reported

- Details of building or land appurtenant there to, or both, being a residential house

- Details of land or building or both not being in the nature of residential house

- Details of listed equity shares

- Details of unlisted equity shares

- Details of other securities

- Details of Capital Contributions in other entity

- Details of Loans & Advances to any other concern (If money lending is not assessee’s substantial business )

- Details of motor vehicle, aircraft, yacht or other mode of transport

- Details of Jewellery, archaeological collections, drawings, paintings, sculptures, any work of art or bullion

- Details of Liabilities of loans, deposits and advances taken from a person other than financial institution.

Schedule SH-2 and AL-2 is applicable for start-up companies.

Conclusion

The New ITR (income tax return) forms notified by the CBDT recently underline the government’s stated objective of increasing the tax net and reducing the possibility of tax evasion. The additional disclosure requirements for companies in ITR-6 as well as directors and share holders in ITR-2 and 3 would help the government in clamping down shell companies. In summary, taxpayers need to be very careful this time and will need to collate additional details/ reporting requirements well in advance this year, in order to be able to fulfil the reporting requirements prescribed in new ITR forms. We also expect greater automated scrutiny of ITRs, based on extensive data/ details required and furnished in ITRs.